Navigating through the mortgage application process can be daunting, especially with the myriad of documents required. To help simplify this journey, we’ve compiled a detailed guide outlining the essential documents needed for a successful mortgage application.

General Documentation

1. Identification Requirements

Two Pieces of ID: Each applicant must provide two forms of identification. These are divided into primary and secondary categories.

Primary Identification:

Options include a driver’s license, passport, Canadian Armed Forces ID, NEXUS Card, or any government-issued document with a photo and signature.

Secondary Identification:

This can be a birth certificate, Certificate of Indian Status, Old Age Security Card, bank card, or a SIN Card, provided you already have a primary ID.

2. Credit Authorization

You need to sign a digital document permitting the lender to check your credit report through agencies like Equifax or TransUnion.

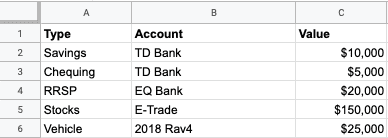

3. Asset List

Provide a simple list of your assets, either in bullet points or a spreadsheet, to strengthen your application. Detailed bank statements may be requested.

Sample Asset List:

- Savings accounts

- Investments

- Real estate

4. Divorce or Separation Agreement

If applicable, provide an agreement between you and your former spouse/partner.

Income Verification

1. Notice of Assessment (NOA)

Issued annually by the CRA, the NOA details your yearly income, taxes paid, and outstanding taxes or refunds.

Where to Get It:

Available from the CRA if you don’t have a paper copy.

2. Pay Stub

For employed borrowers, the most recent pay stub (within 30 days) confirms employment and income details.

3. Letter of Employment

A letter dated within 30 days from your employer outlining your employment details.

4. T4 and T4A Slips

These are tax slips showing your earnings and other incomes like commissions or pensions.

5. T1 Income Tax Return

Required for self-employed borrowers, this document is your complete annual tax return.

Property-Related Documents

1. MLS Listing (Realtor View)

For property buyers, an MLS listing with detailed information is required.

2. Offer to Purchase

This is the contract with the property sellers, provided by your Realtor or developer.

3. Purchase Waiver

A waiver signed upon removing all conditions from the property purchase.

4. 90-Day Bank Statement

Needed if using cash assets for the down payment. It should show a comprehensive transaction history.

5. Gift Letter

If the down payment is a gift, a letter confirming the details of the gift is necessary.

6. Confirmation of Gifted Funds Deposit

Proof that the gifted money is deposited in your account.

For Existing Property Owners

1. Mortgage Statement

A statement from your lender showing all details of any outstanding mortgage.

2. Property Tax Statement

Annual tax statement for each property you own.

3. Sale Agreement

If you’re selling a property, provide the contract for the sale.

4. Rental Tenancy Agreement

For those earning rental income, a copy of the agreement with your tenant is required.

5. Condo Board Letter

If you own a condo, a letter confirming monthly condo fees is needed.

Remember, having all these documents ready can significantly streamline your mortgage application process and improve your chances of approval.